Liz’s view

“Things that were previously held to be sort of unassailable truths are now coming into question,” a16z partner David Ulevitch told me last month. He was making the point that previously uninvestable sectors — like hardware, long ignored by venture capital firms — were becoming attractive because of underlying technological shifts. But the last few weeks have shown that the gloomier inverse is also true.

A generation of kids who learned to code are being supplanted before they’ve even hit their 20s. Enterprise software was the most durable business model of all time, until AI arrived. Loans to those companies were underwritten on the basis of revenue with the assumption that profits would materialize; they didn’t and cans were kicked. In 2007, the thinking was that a mortgage in Montana didn’t have anything to do with a mortgage in Maine; oops.

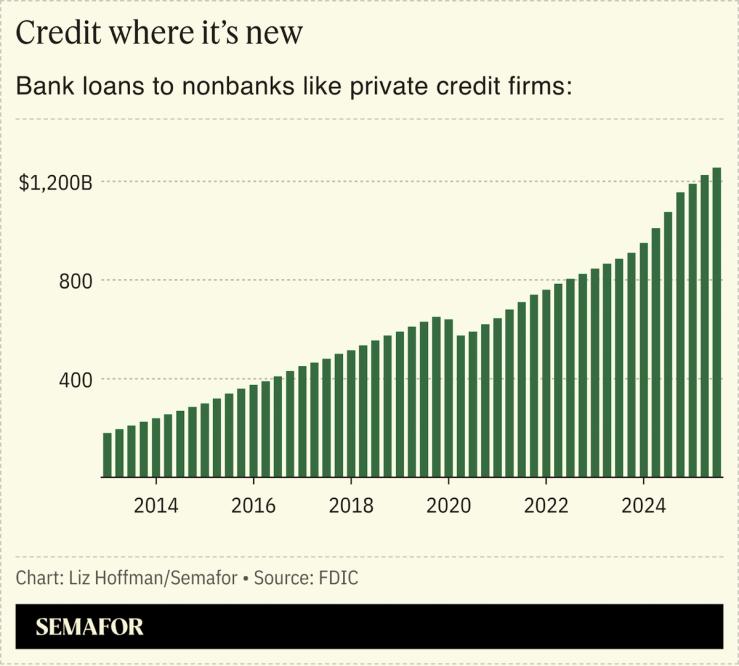

Here’s another one to watch: The fastest-growing type of bank lending over the past decade has been loans to private-credit firms, secured by the value of those firms’ own loans. That $1.3 trillion pot is, as Advent’s managing partner neatly told me a while back, “leverage on leverage.”

The portfolios are diversified, and banks lend 40 or 50 cents on the dollar, which leaves some room for things to go badly before they lose money. But that’s what lenders said about mortgage bonds in the run-up to 2008. They built creaky securities to withstand losses of 10% or so, then watched prices fall by twice that or more.

For the moment, concerns about liquidity in private credit — retail investors want their locked-up money out — have obscured the more important question: are some of the underlying loans bad?

We’ll ask them and hundreds of other CEOs next week about assumptions we’re making today that could prove disastrously wrong. Risk underwriting has the same problem as AI models: garbage in, garbage out.

Notable

- The big banks losing lending business to private credit funds have found a workaround — lending money to those same funds — turning what looked like a zero-sum rivalry into a $4 billion-a-year sideline where Wall Street finances its own disruptors, as I reported two years ago.