Yinka’s view

In recent years Africa’s political and business leaders have come to see Gulf nations as the perfect counterweight to diversify away from Washington and Beijing and tap new sources of capital. That story was less geopolitical fantasy than hard necessity, as traditional funding options dwindled.

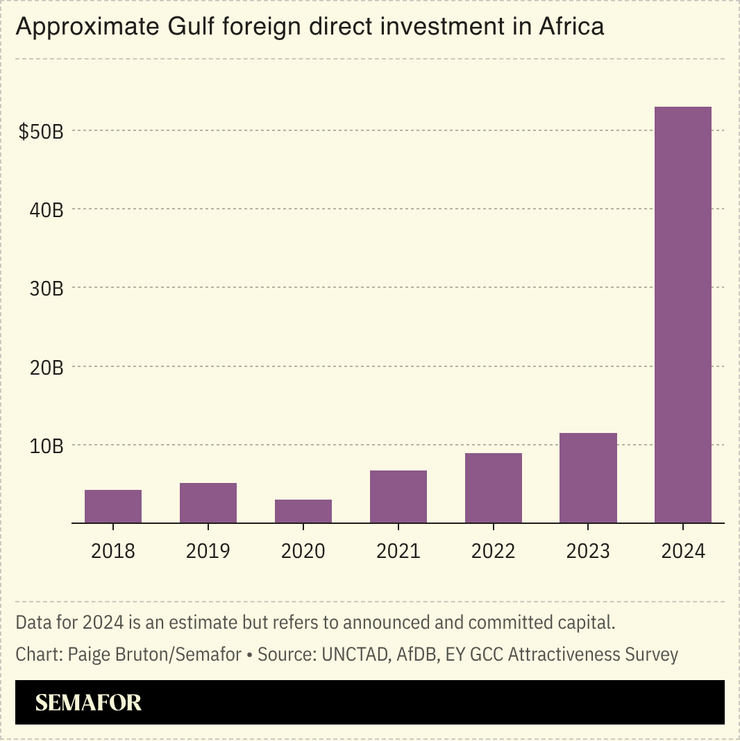

Over the last decade, the Gulf Cooperation Council has put more than $100 billion into Africa across energy, ports, logistics, and tech, dwarfing the US and rivaling Europe. Dubai, Abu Dhabi, and Doha have become regular backdrops for African presidents, ministers, and CEOs. And elites were as likely to fly to the Emirates for financing as to New York or Shanghai.

But that momentum has been severed: The US-Israel war on Iran — and Tehran’s reprisal attacks on Gulf powers — threaten to pull the region’s attention, capital, and political bandwidth back home. As missiles strike cities long assumed to be safe, sovereign wealth funds that have been pouring money into African renewable grids, ports, and startups may soon redirect toward immediate domestic priorities.

Africa is already exposed: Western FDI and development aid has faltered, China has signaled a pullback from large infrastructure loans, and Gulf capital was only beginning to fill that gap. What looked like a reliable “third way” could become another source of uncertainty.

The ripple effects could go further. One analyst told me that Gulf states may reduce support for proxies, security initiatives, and diplomatic outreach in Sudan and the Sahel — shrinking their footprint at precisely the moment Africa faces its own compounding crises.

Diversification away from the West and China was meant to reduce vulnerability. Instead, the continent may discover that in an interconnected world, there is no true hedge — and no partnership is truly immune.

Notable

- Gulf investment is particularly focused on the renewables sector, African Business reported, with Gulf nations hoping to diversify their oil-based economies.