The News

Goldman Sachs will report its worst quarterly earnings in years next week, with a return on equity — a key measure of how profitably it spends shareholders’ money — in the low single digits, people familiar with the matter said.

Writedowns on its GreenSky consumer-lending business, which Goldman is trying to sell less than two years after buying it, and on its holdings of commercial real estate, are likely to exceed $2 billion, people familiar with the matter said.

Goldman has been talking down its quarterly numbers both publicly, as when President John Waldron previewed a 25% drop in trading at an industry conference last month, and privately, as sharp downward revisions in analyst forecasts in recent weeks bear the fingerprints of investor-relations staffers in overdrive.

The poor showing, which is likely to be far worse than modest profit drops at rivals, will ramp up pressure on CEO David Solomon, who is facing heat from inside and outside the firm.

Goldman is beating a hasty retreat from a push into consumer banking that has yielded little but mounting losses, and key partners are voting with their feet. The firm’s relationship with the Federal Reserve, its chief regulator, has deteriorated on Solomon’s watch, people familiar with the matter say, characterizing the Fed’s concern as the firm having done too much, too fast, and without attention to detail.

“The overwhelming share of our time, attention and capital has been in our core businesses — banking, markets, and asset and wealth management. Those are premier franchises.” Goldman’s communications chief, Tony Fratto, said. “Big parts of the business have done really well, and are doing really well, and that’s not by accident.”

Liz’s view

I’ve never cared about Solomon’s side hustle as a DJ, or found the corporate jets especially scandalous. To the charge that Solomon is dictatorial and a bit of a cypher — so what? Neither is a crime, and both can be assets in corporate settings.

But look at the business.

A CEO’s job is allocating resources: capital, people, and intangibles like brand and reputation. Bosses have to spend money on the right things, put the right people in the right seats, and sketch out a vision that brings those people along and leaves the place stronger than they found it. Five years in, Solomon has struggled to do any of that.

The tumult is starting to weigh on the business. Bankers say calls with clients increasingly start with questions about the negative headlines coming out of the firm. Goldman barely kept its M&A crown for the first half of the year, according to Refinitiv, sliding back on top over JPMorgan on the last day of the quarter — an unnerving near-miss at a firm that treats its No. 1 ranking as sacred.

Goldman’s own acquisitions have ranged from middling (United Capital) to disastrous (GreenSky). Solomon has overpaid for things he shouldn’t have (again, GreenSky) and missed out on things that would have moved the needle (Global Shares, which went to JPMorgan, was the last remaining on-ramp into the business of managing employee stock plans, an unflashy but linchpin offering for any firm with wealth-management ambitions).

Solomon approved a brand refresh that would have dropped Goldman’s iconic blue box, at a cost of tens of millions of dollars, people familiar with the matter said. The effort has been pared, a victim of $1 billion in cost cuts targeted for this year. A sponsorship of McLaren survives.

Few of Solomon’s senior personnel moves, whose animating principle has seemed to be there’s no problem an investment banker can’t fix, have worked out.

It’s true that bankers, Solomon’s side of the house, had been in the wilderness for too long under his predecessor, Lloyd Blankfein, a trader. And one of Solomon’s priorities was revamping how Goldman covered its clients; bankers might be better suited than traders, who don’t have clients but rather counterparties. But the track record is poor.

Stephanie Cohen, an M&A banker, was put in charge of consumer banking. She’s now on leave as Goldman gets out of that business. Luke Sarsfield, who had previously counseled healthcare companies on deals, was put in charge of asset management. He was out of that job a few months later.

His co-head, Julian Salisbury, made his name in a small, secretive group that invested Goldman’s own capital. Solomon put him in charge of a giant division that was actively tilting away from that model, toward managing money for pension funds and other clients. He was demoted last year, to chief investment officer.

Another investment banker, Matt Gibson, was elevated to run sales in that business, where he has sparred repeatedly with his co-head, Chris Kojima, people familiar with the matter said. (Fratto said the firm is “on or ahead of target” in its fundraising goals.)

The departure of a string of senior women — Katie Koch, Heather Miner, Margaret Anadu, Dina Powell, Jo Natauri — is starting to harden into a narrative about diversity, a key focus of Solomon when he was campaigning for the job.

Waldron overruled the search committee tasked with hiring a new head of HR in 2020, people familiar with the process said, rejecting their candidate and instead selecting an executive who oversaw talent for Johnson & Johnson’s supply chain business. Bentley de Beyer dismantled and rebuilt Goldman’s review and promotion system in ways that bothered many. He lasted two years, and the system went back to what it had been before.

Say what you will about Goldman, it’s always been pretty well run. Its lingering partnership culture had its shortcomings, which I’ve written about, but it bred a discipline, left over from the days when partners’ capital was at risk.

Solomon moved to corporatize Goldman in ways I’ve mostly defended as long overdue. That meant sharing more of the spoils with shareholders than with employees, and soliciting less input — and tolerating less dissent — from its 400-odd partners.

But he also imported corporate bloat, fueling a sense that nobody has been minding the store. Headcount grew from 39,800 when Solomon took over in 2018 to nearly 50,000 at the peak, before January’s layoffs. Another round of firings last month cut a few hundred expensive bankers, and another round is planned for August or September, concentrated in asset management.

The second quarter is going to be a bad one and unless the dealmaking environment improves by September, so is the third. It’s not inconceivable that Goldman shares dip under $300 this year, at which point Solomon’s armor starts to chip.

Room for Disagreement

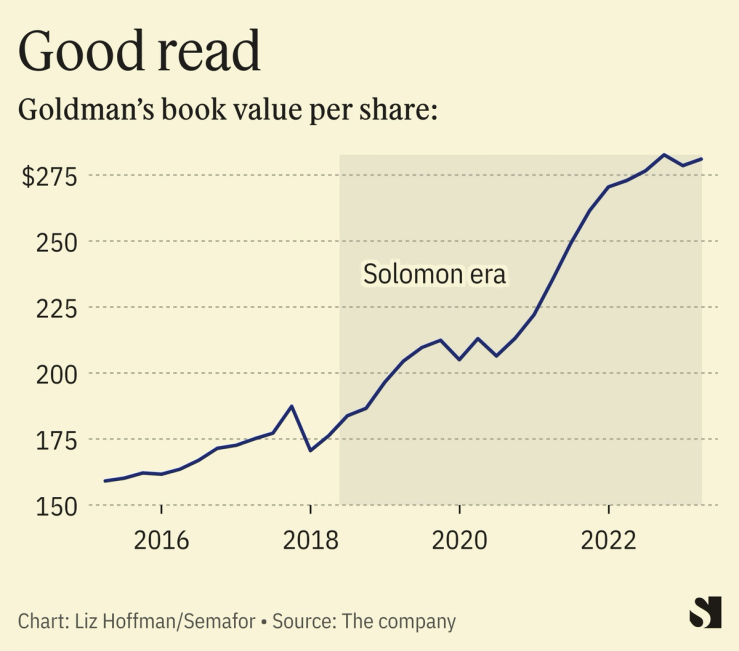

Defending the firm in recent weeks, Goldman’s communications chief Tony Fratto has pointed to the stock price, which is holding steady in the low to mid $300 range. That’s true, and Solomon has steadily grown book value.

The View From Midtown

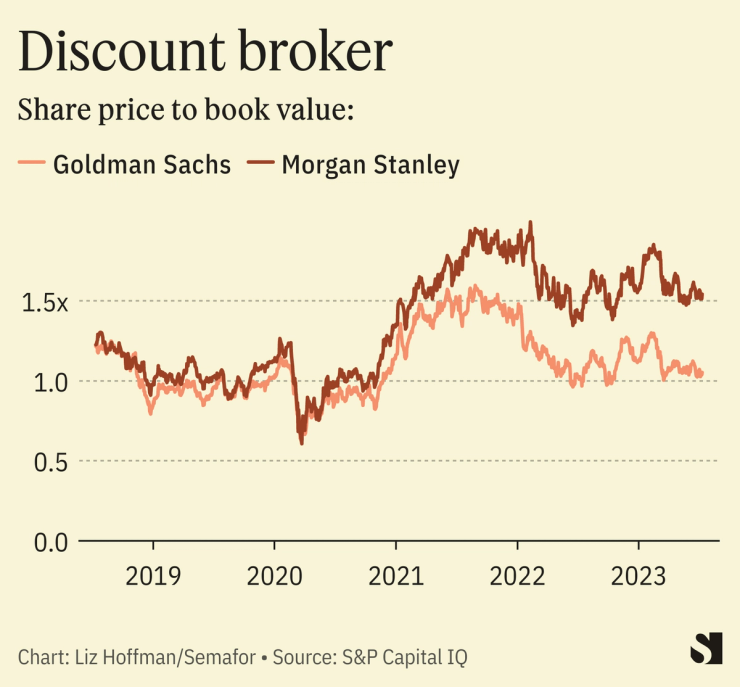

Goldman trades at a widening discount to its closest peer, Morgan Stanley, whose CEO, James Gorman, is in the final year of a model tenure. Morgan Stanley’s acquisitions have paid for themselves and the firm is now Wall Street’s steadiest performer, largely drama-free in both its financial results and its internal workings.

Notable

- Goldman is looking for a way out of its credit-card partnership with Apple, which as recently as a few months ago held up as a win in an otherwise disastrous push onto Main Street, WSJ reports.

Correction

Goldman Sachs maintained its top spot in advising on global deals for the first half of 2023. The story previously misstated that it had fallen to No. 2.