Liz’s view

Private equity is finally eating its vegetables.

For months, markets have been hand-wringing about private credit while quietly ignoring the obvious: equity sits below debt. Always has. “If you’re worried about private credit, and a lot of people are, you should be really worried about private equity,” I wrote in March.

Ninety-eight percent of the loans in Apollo’s flagship private-credit fund are at the absolute top of the capital stack. At Blackstone, it’s 90%. Before these firms lose a dollar, the private-equity firms that own the companies they lent to will see their positions wiped out. It’s called first-loss for a reason.

Now, the cascade of financial loss that happens when companies run out of money is in motion.

Medallia, a software company that runs customer-satisfaction polls, was turned over to its lenders yesterday after being unable to pay its debt. In one of the biggest private-equity goose eggs on record, Thoma Bravo will lose its entire $5 billion equity stake. This is how it’s supposed to work. Equityholders, whether they are PE shops or public stockholders, bear the first loss when things go south. They are rewarded for bearing that risk with unlimited upside when things go well. Lenders, meanwhile, are more protected from wipeouts, but can only get their money back, plus a little interest, if the company thrives.

Equally encouraging is how Medallia’s lenders, led by Blackstone, handled it. For months they allowed the company to pay interest in scrip — a kick-the-can approach that adds to the amount owed rather than collecting cash — but eventually they stopped extending the fantasy of a turnaround. That’s a functioning credit market doing what it should.

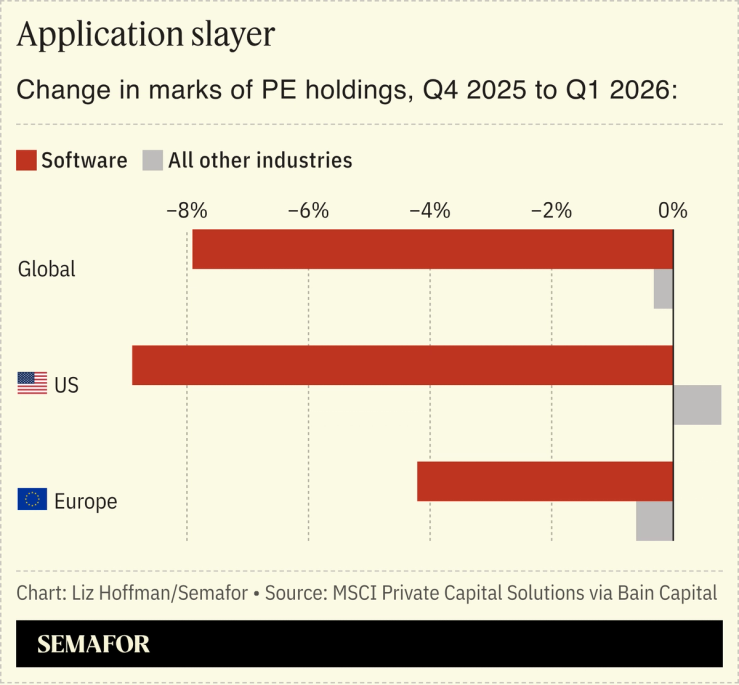

The watchlist for the next Medallia is growing but not alarmingly long. The SaaSpocalypse sentiment is easing, at least in the public markets. The enterprise software industry faces real challenges from AI, and the crop of 2021-2022 LBOs in this space will age badly; keep an eye on Coupa, a 2022 Thoma Bravo take-private, Zendesk, and Hellman & Friedman/Permira buyouts of the same year. But that’s fine. Lenders will take the keys and private equity will take its lumps, as designed.

Notable

- Orlando Bravo is attempting to reassure investors that a poor bet on Medallia is a one-off, and reaffirming that his firm can benefit from AI.