I recently convened an African venture capital roundtable in Cape Town with global corporate VCs and family offices circling the same question: Is African VC the right way to gain exposure to the continent’s upside?

The answer, increasingly, was that the risk was better understood than the upside.

Interest in African venture capital has risen sharply, fueled by a growing cohort of venture-backed companies scaling into underserved markets and a steady stream of exits, from Fawry to InstaDeep. Global exchanges such as the London Stock Exchange are actively positioning to attract high-growth African listings. Corporate acquirers are scanning the continent more systematically. Yet capital remains cautious. Returns data is thin. Risk perception is thick.

The discussion in Cape Town surfaced several reasons for optimism — grounded more in structural reality and less in hype.

Start with the macro paradox. For decades, African economies have struggled to combine labor and capital efficiently. The World Bank has described productivity gains across much of the continent over the past 60 years as “negligible.” That sounds bleak. It is also precisely the opening. Inefficiency creates whitespace. Entrepreneurs are using technology to realign productive costs with affordability in markets long priced out of formal services.

Artificial intelligence only sharpens that opportunity. McKinsey estimates AI could unlock up to $100 billion in annual economic value across African sectors. Also, in fragmented, informal markets, aggregation is power. Technology-driven models that consolidate demand, digitize workflows, or formalize payments can move entire industries up the productivity curve.

Demographics reinforce the case. Africa’s population is young and increasingly urban, with a consumer market projected in the trillions and business demand expected to exceed $4 trillion by 2030, according to research from the Brookings Institution. Unlike more mature markets, there is limited legacy infrastructure and fewer entrenched incumbents.

But the most compelling argument is human capital. The caliber of founders building across fintech, logistics, health, and climate is aligned with global standards.

Liquidity is happening, and will only increase. Exit activity, while still early, is broadening. International acquirers are paying attention. A look in the portfolios of the major African VCs points to more high value exits about to happen.

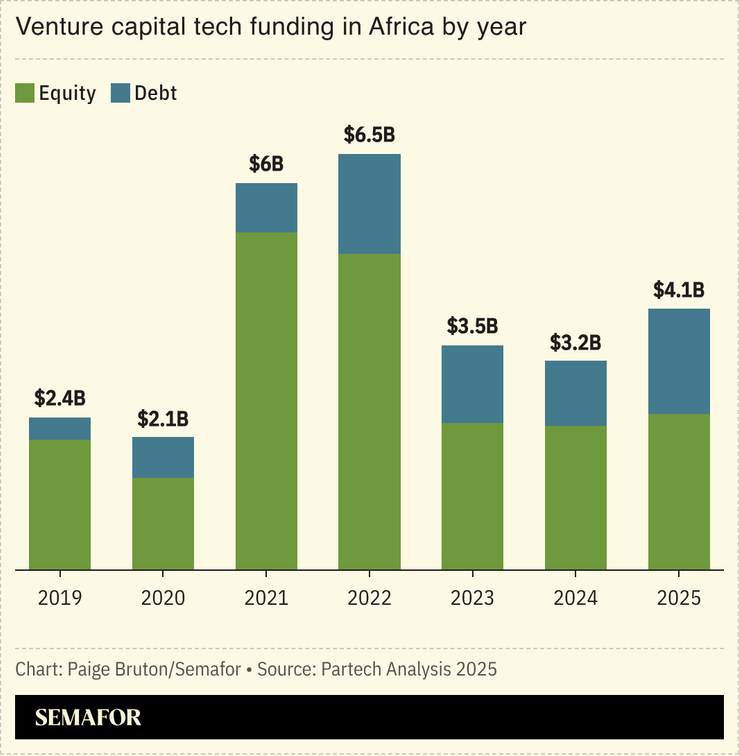

The constraint is capital depth. Venture funding has grown from roughly $100 million in 2015 to more than $3 billion in 2025 — impressive in isolation, but marginal in the global context. Africa still accounts for less than 1% of global VC, despite representing roughly 5% of global GDP and 18% of the world’s population.

Global investors want more evidence of realized exits. The ecosystem is only now generating consistent data sets that institutional investors recognize. Until that track record compounds, capital will remain selective.

Africa’s capital stack is unusually diverse. Impact funds, development finance institutions, family offices, corporate VCs — each with different mandates and return expectations. For founders, that can mean fragmentation. For the ecosystem, it reinforces the central role of specialist VCs who operate across stages and can actively orchestrate pathways to scale and exit.

The task ahead is straightforward but urgent: sharpen the data, clarify the risk, and quantify the upside. Africa’s startup ecosystem does not need a narrative premium. It needs a measurement premium.

The opportunity is real. The question is whether global capital is prepared to price it correctly — and whether African VCs can continue building the evidence to make that case undeniable.

Maurizio Caio is the Nairobi-based founder and managing partner of TLcom Capital.