Yinka’s view

For 25 years, the defining logic of China-Africa trade has been simple: Africa exports raw materials, China manufactures products, and Africa buys them back.

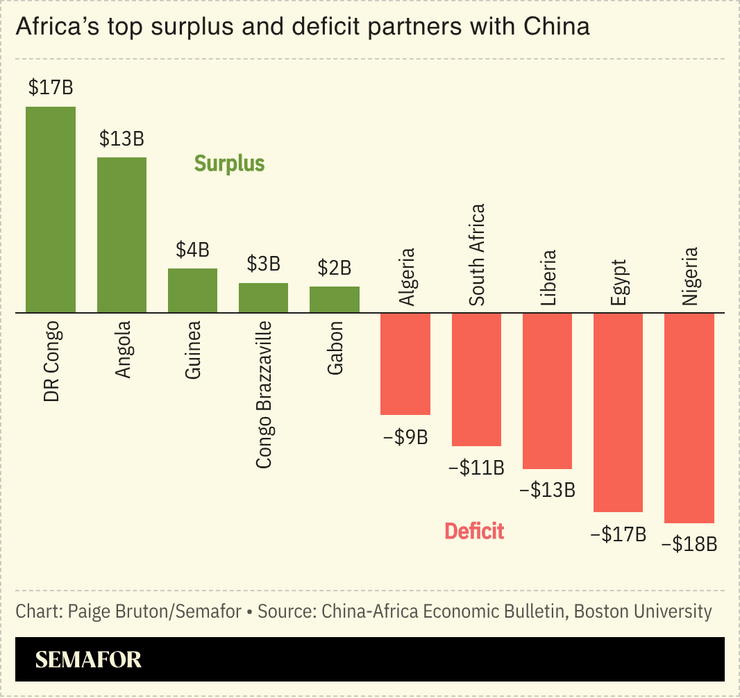

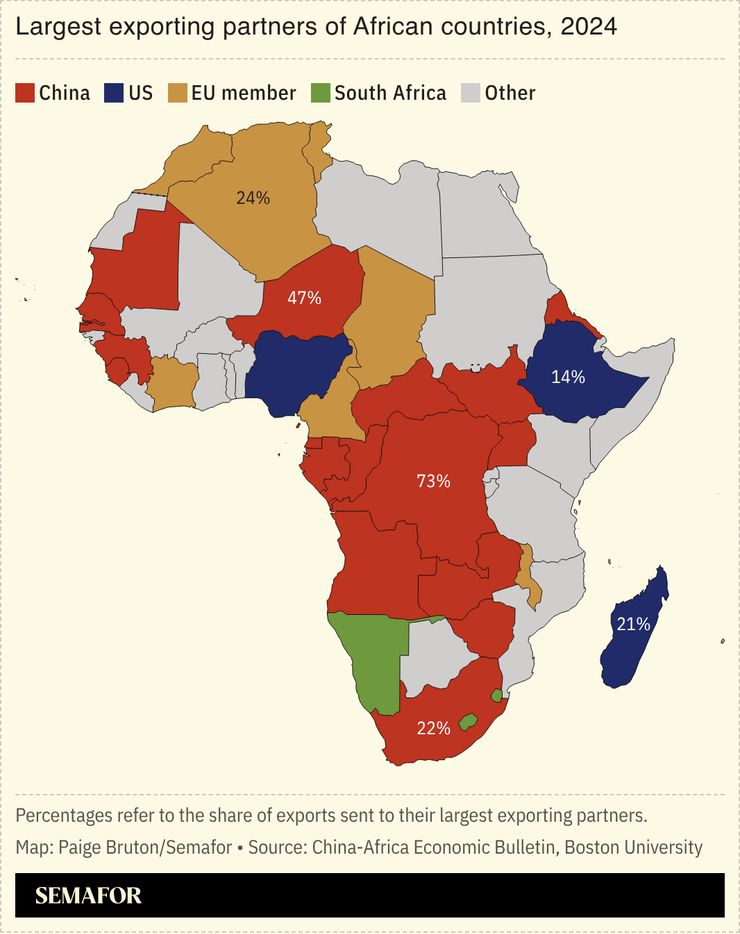

In 2024, that arrangement led to a record $275 billion in trade. African countries imported $182 billion worth of Chinese goods while exporting just $93 billion back, overwhelmingly in raw commodities, according to a recent report from the Boston University Global Development Policy Center and the African Economic Research Consortium.

Yet the same data reveals a shift that many observers still underestimate: China may need Africa more than the established narrative suggests.

African countries supply more than 80% of China’s chromium and manganese imports. Guinea alone provides roughly a third of its bauxite. Copper exports from DR Congo and Zambia continue to expand. These are not niche commodities. They are critical inputs for electric vehicles, batteries, and the clean-energy supply chains on which China is staking its industrial future.

That dependence gives African governments more leverage than they have historically exercised. Zimbabwe’s restrictions on raw lithium exports, which pushed Chinese investors toward local processing facilities, offer an early example of how resource-rich countries can use market access to bargain for more value addition at home.

But a second trend is moving in the opposite direction.

The era of large-scale Chinese infrastructure lending is over, note the report authors. At the peak of the Belt and Road Initiative, Chinese loan commitments often exceeded those of the World Bank. Today, new lending from Beijing has fallen below $5 billion a year. More strikingly, African countries now repay more to Chinese lenders annually than they receive in fresh financing, making China the only major creditor with net negative capital flows to the continent.

The consequences are becoming visible in government budgets. Between 2026 and 2030, African countries are projected to spend 11% of public revenues on debt servicing. In Angola, the figure reaches 42%; in Senegal and Djibouti it exceeds 25%.

That is the central tension in the next phase of China-Africa relations. Africa’s bargaining power is rising just as its fiscal space is shrinking. Countries that can use mineral leverage to attract processing and manufacturing investment — while avoiding debt burdens that crowd out industrial policy — will be best positioned to move beyond the role of raw-material supplier.

Notable

- While the US has sought to increase tariffs on Africa over the last year, China has scrapped duties on all but one nation.