Tim’s view

With peace talks between Iran and the US in limbo, one of the main questions looming over global energy markets is why the price of oil isn’t much higher than it is.

Prices ticked down on Tuesday after US President Donald Trump insisted talks were ongoing, contradicting an earlier report from Iran’s state news agency. They are now hovering around $95 per barrel, 30% above pre-war levels. But given that we’re now into the fourth month of the biggest supply disruption in history, it feels remarkably mild. Natasha Kaneva, head of commodities research at JP Morgan, pondered in a recent note whether the fact this crisis has “felt oddly more manageable” than the post-Ukraine invasion crisis of 2022 is an indication that the world actually just needs significantly less oil than most people thought. Still, we’re far from being out of the woods.

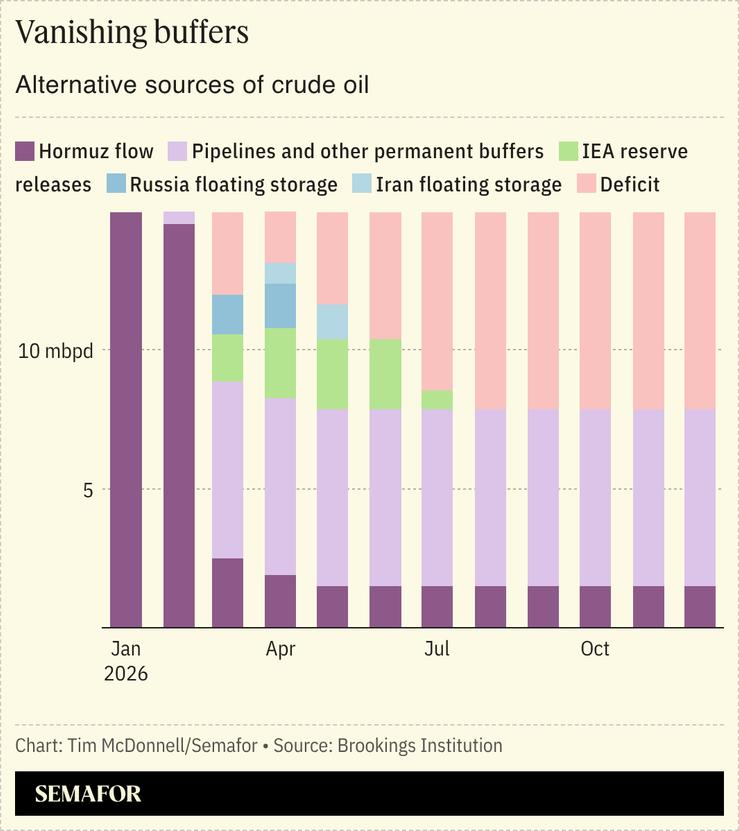

A few factors have helped to keep prices relatively in check. The UAE and Saudi Arabia were able to push crude through pipelines that bypass the Strait of Hormuz. China, which had been on a stockpiling spree, slashed its buying. In fact many countries went through a spasm of panic-buying at the beginning of the conflict, which has since cooled off. The US and others tapped strategic reserves, US exports hit a record high, temporary waivers on some sanctioned Iranian and Russian crude unlocked more frozen barrels, and a handful of tankers have managed to slip through the strait. On top of all that is demand destruction: People use less energy when it’s expensive, so high prices beget lower ones.

The question is how long all these buffers can last relative to the pace of ceasefire talks. Robin Brooks of the Brookings Institution made a useful forecast showing that in May, the various buffers added up to enough crude to cover all but about 3.3 million barrels per day of what used to flow through the strait. But that gap is set to double to 6.4 million by July. $150, Brooks concludes, is still very much within reach, a sentiment repeated Friday by a senior ExxonMobil executive.

Some version of that future appears to be locked in already, since Tehran has indicated it will need at least 30 days from the signing of a ceasefire to facilitate the return of pre-war flow levels through the strait. And that’s a hopeful timeline, given the hurdles of demining, returning confidence to captains and insurers, and bringing in a legion of empty tankers to stock up — and the risk that one errant drone could reset the whole process to square one.

“With all due respect to the optimism that continues to be shown in trading markets, we haven’t even peaked,” veteran analyst Bob McNally said Friday on the (excellent) Oil Ground Up podcast. “Things haven’t even stopped getting worse, let alone getting better.”

Notable

- Compared to past economic crises, demand for oil has fallen significantly, CNN wrote, by at least 4.3 million barrels per day. By comparison, during the 2009 financial crisis, oil rose above $140 a barrel and yet demand destruction was just 2.5 million barrels per day.