The Scene

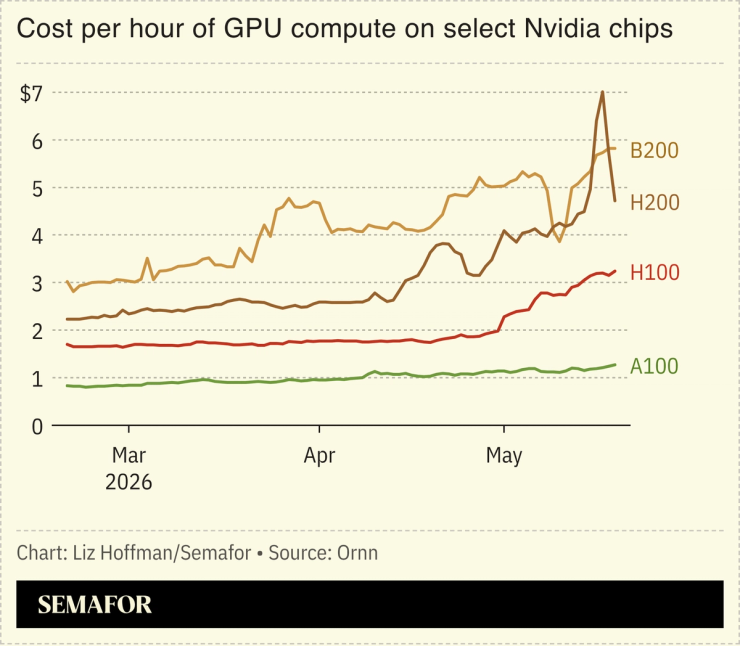

The cost to rent Nvidia’s cutting-edge Blackwell chip for an hour has doubled since February. Where it goes next is Wall Street’s latest obsession.

Financial heavyweights and startups are building out a futures market for compute, providing a way for traders to buy and sell the processing power that underpins AI at a predetermined price in the future — much like the way they bet on the fluctuating price of a barrel of oil.

“Compute is going to be the next big commodity in the world,” said Wayne Nelms, the 22-year-old co-founder of compute pricing-data startup Ornn, which is named for a League of Legends God, and just inked a deal with the owner of the NYSE owner Intercontinental Exchange.

ICE and rival exchange CME Group have both announced plans to launch GPU futures, a market BlackRock CEO Larry Fink has called “a new asset class.” Evangelists say these efforts could rival the $6 trillion energy market and let industry participants hedge their risk against the rising demand for computing power.

As AI rewires the economy, every company becomes a “wrapper” for the computing power it holds, said Nelms, whose startup, founded last year, has eight employees. “Your input will be tokens and your value to shareholders is what you can build on top of that raw compute. That means that potentially every company in the world is a participant in this market.”

Know More

The closest analogies for compute are oil and electricity — commodities that are essential, volatile, and hard to store or transport, Silicon Data CEO Carmen Li told Semafor. While there’s enough price uncertainty to sustain a two-sided market, compute tends to depreciate in real time as new chips are rolled out. A GPU futures market helps connect players like CoreWeave, which rents out access to GPUs and needs to hedge against falling prices, with hyperscalers like Meta and Google that are impacted by rising prices. (AI-native startups that need tokens but can’t afford long-term contracts fall into this bucket, too.)

A futures market for compute would also invite big market-makers like Citadel Securities and Jane Street, and, inevitably, speculators looking for another way to bet on the AI boom.

“It’s like trying to establish the next West Texas Intermediate, a crude-oil analog for compute,” said Brett Harrison, a former Jane Street and FTX US executive whose exchange operator, called Architect, runs a futures market dedicated to compute trading and licenses Ornn data for some of its products.

West Texas became, along with the North Sea’s Brent oilfield price, the benchmark for oil markets in the 1980s and 1990s and set off the largest commodity bazaar in history.

Silicon Data’s Li told Semafor she’s less interested in retail traders, though the company’s prices are already used to resolve bets among Polymarket users. “This has to be a functional, usable product, not a casino,” she said.

(You can, of course, already bet on the price of compute on prediction markets, with speculators on Kalshi assigning a 40% chance that Nvidia’s B200 chips rent for at least $5.91 an hour this coming Friday.)

Step Back

Enabling a GPU futures market is the real uncertainty about what compute will cost down the road. Technology tends to get cheaper over time, but AI boosters say demand will grow faster than data centers can be built and chips manufactured. Memory shortages are pushing prices up, while the power of next-generation chips raises questions about the lasting value of older ones.

“When we started this business, everyone asked us why [the cost of compute] would ever go up,” Nelms said. But even the price of Nvidia’s older workhorse H100 Hopper chip has risen 63% over the past month, according to Ornn’s data. That’s a steep enough rise to give heartburn to CFOs already dealing with soaring token budgets.

Liz’s view

Not everyone will cheer the financialization of a resource that AI companies are already struggling to secure. If you think the public is mad about AI, just wait until the stories start about how much money Wall Street is making from paper bets on it.

But this is what futures markets are for: surfacing prices, distributing risk, and forcing competing views into the open. And AI right now is little but competing views. The long arc of technology bends toward abundance and lower prices. But AI’s bottlenecks — power, capital, chips, transmission — are real. The CEO of a major data-center operator told me recently that LLM companies are “massively, massively underpricing” tokens. Regulation is coming, too, which rarely makes anything cheaper.

The biggest hurdle for this nascent market is that compute is an oligopoly and the oligopolists are doing just fine. In fact, hyperscalers like Meta and Google “benefit from opaque pricing and kind of bundled pricing,” Don Wilson, DRW’s founder, told Odd Lots last year. Without their participation, the futures market will never get off the ground. Oil futures work because drillers, refiners, and shippers all use them alongside speculators. (Airlines, to their current regret as prices spike, do not.) Without commercial users, you don’t have price discovery. You have gambling.

The fact that CoreWeave, whose co-founders ran energy hedge funds before seizing on GPU rentals, doesn’t have a humming compute-trading desk suggests that takeup might be slow from the big players. Without it, this will remain the casino that Li is trying to avoid.

Room for Disagreement

A futures market could level the playing field and prevent big tech firms from running off with the AI crown. Investors might take a risk on a smaller player, and banks might lend to a challenger, if they know they can hedge their biggest risks. “The cost of financing is so difficult right now because no one knows how to measure risk in this space,” Li said.

There are also still questions about the quality of pricing data because neither Silicon Data nor Ornn have access to the closely held contracts between the biggest players like Google and Meta. Instead the startups rely on spot prices from smaller “neoclouds” like Crusoe and Nscale, which tend to be more volatile.

This article has been updated to reflect a commercial partnership between Architect and Ornn and to note that Architect is not itself an exchange but an exchange operator.

Notable

- DRW’s founder thinks GPU futures is the next big market.

- Compute “looks a lot like oil in the 1970s: a bottlenecked resourced begging for financialization,” Substacker Dave Friedman writes.