Alaa’s view

Saudi Arabia’s sizable first-quarter budget deficit has been widely read as an early sign of the Iran war’s toll on the biggest Arab economy. That’s a fair assessment, but only half the story. What most takeaways missed is that the widest quarterly shortfall since late 2018 also reflected, to a degree, a policy choice.

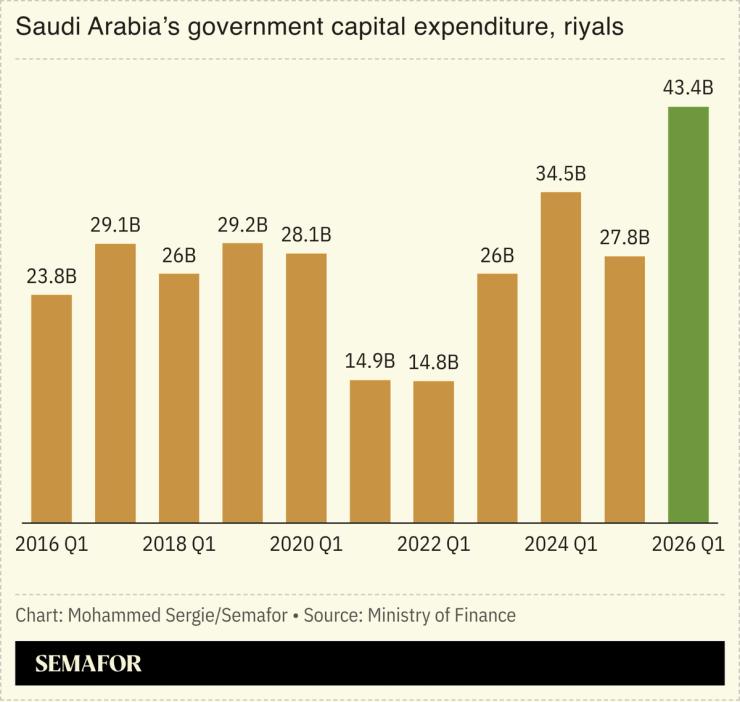

As oil exports slumped in March after the closure of the Strait of Hormuz, my understanding is that policymakers accelerated investments to support the development of alternative trade routes to mitigate the impact on domestic and regional supply chains. That helped drive the largest first-quarter capital expenditure in at least a decade.

Part of the calculation was surely financial. The 3% drop in oil revenues during the period was partly due to low average prices in the first two months of the year, as well as standard payment lags. Going forward, higher prices, coupled with the kingdom’s ability to ensure a big chunk of hydrocarbon exports still reach customers via the East-West pipeline, will probably more than offset the lost barrels.

But the second part of the calculation was trickier. Faced with a choice between waiting for more clarity or taking action that would consume 75% of the expected full-year deficit, the government judged that the cost of doing nothing could be higher.

The somewhat risky approach is seen by many investors as encouraging. During a recent trip to Riyadh, a key concern that bankers and economists shared with me was whether the non-oil economy could absorb the war-driven uncertainty, which was emerging just as the kingdom’s sovereign wealth fund recalibrated its priorities and scaled back spending on certain projects. At a time when private businesses would be understandably reluctant to invest, the state should pick up the slack.

The budget confirmed that. While the 26% increase in defense outlays was hardly surprising, it was notable that capital spending, which is typically soft at the start of the year, jumped 56%. Subsidies also rose sharply, partly because pump prices remained steady, according to Monica Malik, chief economist at Abu Dhabi Commercial Bank.

Ziad Daoud, chief emerging market economist at Bloomberg Economics, estimates that the conflict is costing the kingdom about 1.5% of GDP each month, but that the bill is probably higher for most of its neighbors.

Because Saudi Arabia is the only Gulf country that publishes timely national accounts, we also know that the intervention did help to buttress the economy in the first quarter. Headline GDP grew by 2.8%, with non-oil industries growing at the same pace. Government activities rose 1.5%, having contracted in the last three months of 2025.

Yet, despite what some might consider an eye-watering spending increase, the government may still end up with a lower budget deficit for the year as a whole than last year’s 5.8% of GDP.

“We still see scope for a smaller full-year deficit,” ADCB’s Malik wrote in a report. “We expect stronger oil revenue in subsequent quarters, given the marked rise in oil prices and Saudi’s ability to divert a significant share of its crude exports.“Alia Moubayed, chief MENA economist at Jefferies International, also noted that the shortfall in the first quarter was driven by “exceptional expenditure, some of which will have a multiplier effect on growth.”

This may explain why credit markets barely budged after last week’s spending figures. The cost of insuring Saudi debt actually dropped by three basis points at the time of publication on Thursday, while the yield on the government’s ten-year dollar bonds was little changed, according to data compiled by Bloomberg.

Moubayed said that a reopening of the Strait of Hormuz could help lift exports of crude and refined products to 7 million barrels a day. At an average price of $90 a barrel, this could bring the budget shortfall to 3.7% of GDP even with a 10% annual rise in government spending.

This scenario requires a resolution to the conflict that would allow trade and oil flows back through the strait. Without that, the government’s challenge would be to curb spending to keep the deficit in check, she said.

That adjustment, however, would not be unique to Saudi Arabia or the Gulf, nor would budgets be the biggest thing to worry about.

Alaa Shahine Salha is a senior executive at Saudi Research & Media Group and an economics contributor for Asharq Business with Bloomberg. He previously served as Bloomberg News managing editor for the Middle East and managing editor for economics in Europe.

Notable

- The Iran conflict has hit the foundations of the Gulf economies. While they can cope with the estimated $200 billion repair costs, it will be harder to repair the damage to the reputation for stability, writes Masha Kotkin for the Stimson Center.