The Gulf’s construction market was worth $175 billion in 2025, built on gigaprojects and other oil-funded diversification plans; the war has put much of that on pause.

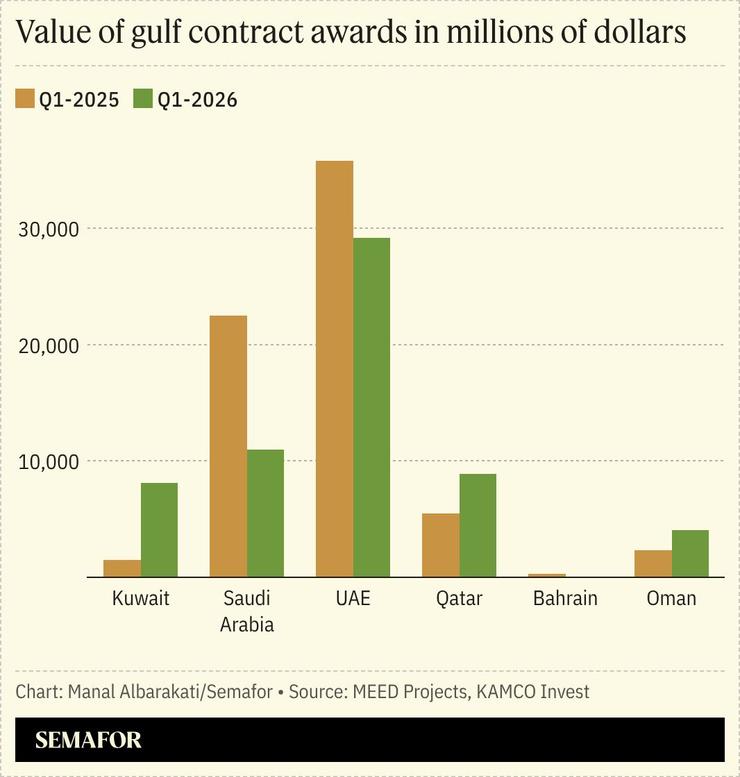

The number of contract awards across the region fell from 80 in February to just 25 in March, with their value dropping from $26 billion to $11.8 billion, according to MEED Projects data cited by Kamco Invest, a Kuwaiti investment firm. Saudi Arabia, which accounts for nearly half of the region’s $2 trillion project pipeline, saw awards fall 51% year-on-year in the first quarter of 2026. The even bigger UAE market also saw a significant fall.

The numbers are telling of something broader than a single bad month: The Gulf’s construction boom has always been primarily funded by oil revenues. Disruptions to the Strait of Hormuz and attacks on energy infrastructure since Feb. 28 have affected both production and exports, straining government budgets, disrupting supply chains, and making investors wary. Whether the projects now on hold or moving more slowly ever get built depends on what postwar priorities look like. Kamco says project activity is likely to remain “sluggish” through the rest of this year, but suggests a bounce-back is possible in 2027.