As we scooped last week, bankers have been puzzling over how to handle the tsunami of selling — more than $1 trillion at the valuation being discussed — that would hit the market six months after the IPO, if the company pursued a traditional insider “lock-up.” They are considering ways to have those shares trickle into the market sooner and more slowly, assuming the demand is there.

A document prepared by hedge fund Lykos Global Management that was seen by Semafor and shared with some of SpaceX’s underwriters pitches a new IPO structure and games out how it would work for a company SpaceX’s size. (It’s unclear whether SpaceX is considering this structure, but Semafor reported that similar ideas are on the table.)

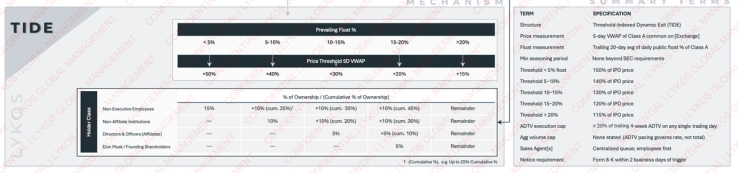

If SpaceX stock price trades at a five-day average that’s 50% higher than the IPO price, the first gate would lift, allowing employees to sell 15% of their stock, according to Lykos’ presentation. After that, the price thresholds decrease because the market is deeper and can more easily absorb new shares without wild swings.

Lykos Global Management presentation, reviewed by Semafor

Lykos Global Management presentation, reviewed by SemaforA sustained 40% increase over the list price frees up employees to sell another 10% of their shares and lets SpaceX’s non-affiliated venture investors sell 10%. Directors at the company are let out later, then finally CEO Elon Musk, though whether he wants to sell remains an open question.

The process — dubbed the Threshold-Indexed Dynamic Exit, or TIDE — is cheekily named to fix the problem it solves: the wave of selling that follows big IPOs and can weigh on the stock price. It’s essentially a rolling IPO, calibrated to the market’s ability to smoothly absorb the largest chunk of stock ever thrown its way.