Alaa’s view

The way Egypt is handling the economic fallout of the Third Gulf War suggests that the country has learned from past mistakes. Unfortunately, that may not be enough.

The conflict, by my count, is the fourth man-made shock to hit the economy since the Arab Spring 15 years ago. Those crises required two large IMF deals supported by tens of billions of dollars in Gulf aid and investments, reflecting a long-standing view among Gulf capitals that stability in the most populous Arab country is key to preventing wider turmoil. In 2023, the UAE alone pledged more than $30 billion as part of an IMF-backed global bailout.

A month into the Iran war, Egypt finds itself one of the economies most exposed to the war outside the Gulf. A net energy importer, it has been hit by higher prices and a suspension of Israeli gas supplies, adding to pressure from hot money outflows. The pound was among the world’s worst performers against the dollar in March.

Still, allowing the currency to act as the first shock absorber marked a departure from the usual script — one that in past crises made matters much worse. The pattern was familiar: burning through buffers in a futile defense of the currency, leading to crippling dollar shortages and a spike in inflation. Delaying unpopular policies only made the eventual adjustment much more painful.

When the US and Israel attacked Iran, policymakers in Cairo were in the final stretch of an IMF program expanded after the Gaza war. Inflation had eased, public finances were improving and foreigners had parked more than $30 billion in Egypt’s debt market. Remittances boomed as the diaspora regained trust in the system.

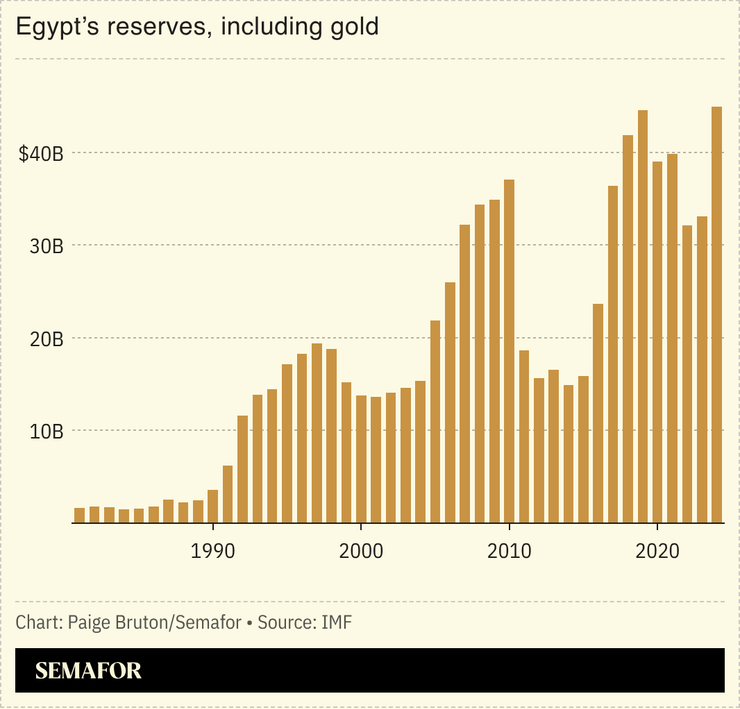

Authorities resisted the temptation to use record foreign reserves to defend the pound, even as the conflict sparked a sell-off across emerging markets. The government also moved quickly to slash fuel subsidies. These measures earned Egypt praise from the IMF and global investors.

“You could see that investors took note of the change,″ said Mohammed Abu Basha, head of macroeconomic analysis at regional investment bank EFG-Hermes. Even though around a third of “hot money” left during March, he said it could have been worse. “The attitude is different,” he added.

There are other reasons to stay positive. Unlike past crises, there are virtually no signs of a black market for dollars. Goldman Sachs doesn’t expect domestic confidence in the Egyptian currency to be shaken anytime soon. In a recent note, the bank said even under its most severe downside scenario, Egypt’s financial buffers were not expected to approach the lows that followed Russia’s invasion of Ukraine.

And yet, the war has — once again — exposed long-standing structural weaknesses in Egypt’s external balance, notably the struggle to develop enough stable sources of foreign income.

Tourism revenue had rebounded before war broke out. In real terms, however, it hasn’t moved decisively beyond its pre-2011 peak, an unimpressive feat for a country with Egypt’s potential. Steep currency devaluations over the past decade have not produced the kind of durable export booms policymakers hope for, reflecting difficulties in developing competitive sectors. Add Egypt’s food import bill, and its shift from being a net oil exporter to an importer, and the result is a chronic trade balance deficit.

Not all of this can be fixed through policy. Attacks by the Iran-backed Houthi rebels in Yemen in 2023 significantly curtailed Red Sea shipping, slashing Egypt’s revenue from the Suez Canal. Political turmoil can also partly explain tourism volatility, but not why Egypt has been repeatedly taken to arbitration by international investors.

Left unaddressed, these vulnerabilities risk turning every geopolitical shock into a perfect storm.

In 2017, a year after securing a $12 billion IMF bailout, a former government official privately predicted Egypt would be a repeat customer soon enough. When I asked why, he said that while Egypt had mastered the mechanics of monetary and fiscal reforms, anything beyond that remained elusive. He was proven right six years later.

What does this mean in terms of the impact of the Iran war? Much depends on its duration. Having to go back for another IMF-funded program due to an external shock would be unlucky, but not entirely surprising.

Alaa Shahine Salha is a senior executive at Saudi Research & Media Group and an economics contributor for Asharq Business with Bloomberg. He previously served as Bloomberg News managing editor for the Middle East and managing editor for economics in Europe.

Notable

- Egypt’s economy quickly began to feel the impact of the Iran war, with sharp stock market declines and natural gas imports being curtailed, reported The New Arab.