The Scoop

The largest U.S. banks didn’t submit a bid for Silicon Valley Bank over the weekend, largely because they were initially excluded from the sales process by the Federal Deposit Insurance Corp. and ran out of time as a result, people familiar with the matter said.

The agency, which is led by FDIC Chair Martin Gruenberg, who has been publicly critical of consolidation in the industry, eventually allowed the biggest global banks into the auction where potential bidders didn’t get access to SVB’s financial information until late into the weekend, when the data room was opened, the people said.

Bids were due Sunday afternoon — too late to ensure a deal could be announced before the market opened on Monday. The four largest U.S. lenders — JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo — are already big enough that they would need a regulatory waiver to buy another deposit-taking bank.

After rejecting at least one bid, the FDIC is now renewing efforts to find a buyer for SVB, taking a second stab at a process that has rattled the financial system and been criticized as muddled and politicized the longer it has gone on.

Know More

Markets had expected a sale of SVB, which was taken over by the FDIC on Friday, by Monday morning. Instead, regulators promised to make its depositors whole and offered a spigot of cash to other troubled lenders — but not a clean resolution to SVB, which became the second-biggest bank failure in U.S. history after a drain in deposits and huge losses in its bond portfolio.

Over the weekend, some potential buyers demanded what amounted to an interest-rate guarantee from the government, some of the people said. They noted that SVB’s losses depend on how quickly and how far the Fed raises rates in its fight against inflation because rising rates make bonds less valuable.

Treasury officials considered using a government slush fund called the Exchange Stabilization Fund to plug the hole, but the idea was dismissed as too complicated and legally iffy, those people said.

The new protections for SVB’s depositors should give more flexibility to regulators in considering bids that request loss-sharing agreements with the government or other similar conditions, people familiar with the matter said.

Liz’s view

Regulators will be dealing with M&A to resolve this crisis sooner or later.

The efforts announced Sunday night to shore up the banking system should keep troubled regional lenders afloat for now by offering them cash to give to panicked depositors. But it will leave them far less profitable, almost ensuring they will eventually need to be sold to giants.

As depositors pull their money, banks can take bonds they own to the Fed and, in return, get the money they need to meet withdrawals. But the government hasn’t explicitly guaranteed that deposits over the $250,000-per-customer insurance cap are safe at other lenders. In other words, the government is agreeing to fund the bank run.

Banks profit on the gap between the interest they pay depositors and other creditors and the interest they collect from the people and companies they lend to.

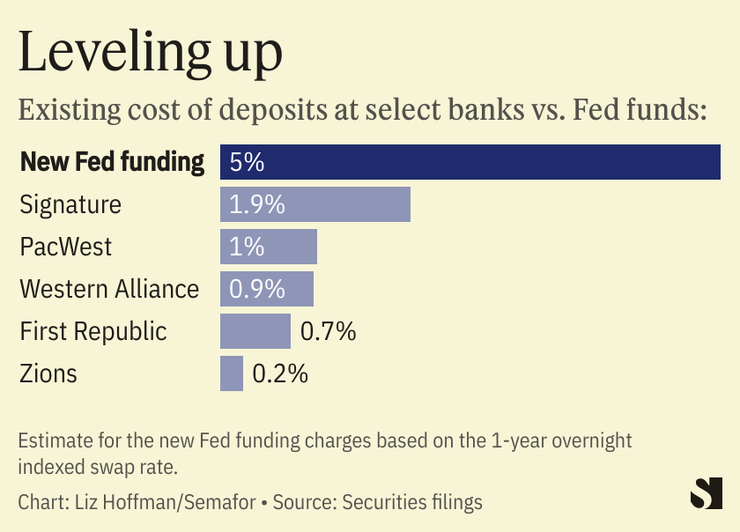

The firms under the most pressure — a growing list that includes First Republic, Western Alliance, and Utah-based Zions Bank — were paying between 0.23% and 2% in interest on their deposits at the end of last year, according to securities filings. If those deposits continue to flee, they’ll be replacing them with government funds charging roughly 5% in interest.

Replacing cheap deposits with more expensive government money will narrow or in some cases entirely close that gap. Profits will evaporate, and these lenders’ shares will trade at steep discounts.

Room for Disagreement

Cam Fine, who ran the Independent Community Bankers of America, agrees that the past week’s events will push smaller banks to merge into bigger ones but says that’s bad news.

“Small businesses are the drivers of job creation. And community banks are the drivers of small business creation,” he said, noting they account for nearly two-thirds of loans to small companies and much of the country’s agriculture lending. “So while regulators may have averted short-term pain, they may have inadvertently inflicted long-term pain.”

Step Back

Nobody looks good here. The bulk of the blame, of course, belongs to SVB’s executives, who badly mismanaged their risk and plowed a surge of deposits into longer-term bets.

But the Federal Reserve Bank of San Francisco was the primary Washington regulator for SVB, Silvergate (wound down last Wednesday), and First Republic. The watchdog has been at the forefront of pushing climate change as a financial risk, holding conferences and writing papers on the issue — a focus that critics say distracted it from its day-to-day bank oversight duties.

Former policymakers who crafted and implemented post-2008 changes are also under the microscope. Former congressman Barney Frank — the Frank in the landmark Dodd-Frank financial reform legislation — was on the board of Signature Bank, which served the crypto industry and failed on Sunday. A former Treasury official under Barack Obama’s administration, Mary Miller, was on SVB’s board.

The View From London

SVB’s London arm, which was seized and sold to HSBC over the weekend for £1, was minuscule compared to its far-reaching influence in Silicon Valley. But it was one of the few sources of venture debt in Britain, which has 49 unicorns, according to CB Insights. It’s unclear if HSBC will continue offering that to its new clients. “The new panic among my portfolio companies is not if they can’t access the money in their accounts, but if they can still tap the debt facilities they were relying on,” said one London-based venture capitalist.

— Bradley

Now What?

Regulators hope bids will come in over the next few days, ideally one for the entire firm. SVB’s loans could be sold to a private-equity firm separately from its deposits (which have to go a bank); Apollo is said to be looking, according to Bloomberg.

Meanwhile, the CEO of the new, government-controlled SVB emphasized in a note to clients Monday that all new deposits, not just old ones, are insured — suggesting the FDIC’s focus is on preserving franchise value for potential buyers.

Notable

- SVB’S customers based in China face more obstacles in opening new U.S. bank accounts elsewhere, leaving them scrambling, The Information reports.