The Scoop

The fallout from the collapse of Silicon Valley Bank — the second-largest bank failure in U.S. history — spread on Friday as tech companies scrambled to make payroll, investors worried about contagion, and other businesses discovered surprising connections to the lender.

Regulators shut down SVB, the country’s 15th-largest bank, after depositors pulled their cash and mounting losses on bond investments made it functionally insolvent. The U.S. Federal Deposit Insurance Corporation transferred insured deposits at SVB to a newly created entity and will now look to sell or wind down the bank.

Startups that kept deposits at SVB held emergency meetings on Friday on how they would meet payroll obligations. Other businesses that aren’t clients of the bank got pulled into the drama.

“I thought I had nothing to do with SVB,” said Kevin Yun, co-founder of GrowSurf, a customer-referral software company that does its day-to-day banking at Mercury, another bank that caters to startups.

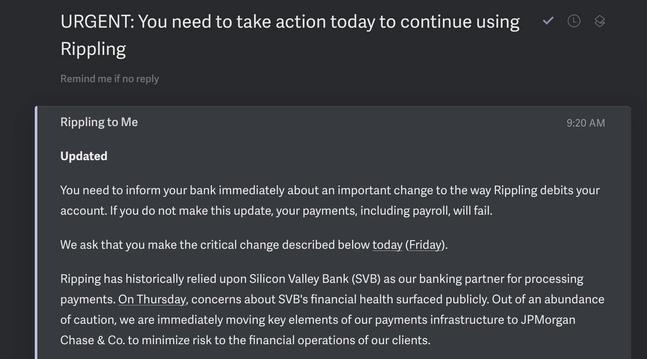

He and hundreds of other startup founders got an email this morning from Rippling, a payroll processor that used Silicon Valley Bank to cut its checks, saying it was moving its accounts to JPMorgan.

In this article:

Know More

The FDIC took over after SVB’s efforts to raise around $2 billion from investors failed. The lender has been hit by both a drop in deposits and a fall in the value of $91 billion in bonds it bought at the worst possible moment, just before interest rates began rising. It sold a chunk this week in a fire sale, crystallizing a $1.8 billion loss.

SVB needs about $15 billion, industry players said, which leaves a limited number of saviors. The largest banks like JPMorgan, which played that role in 2008 and lived to regret it, would need a waiver from regulators to get any bigger. Private-equity firms are flush with cash but rules prevent any one of them from owning more than 25% of a bank, and joint deals are hard to pull off.

Deposit accounts up to $250,000 are insured by the FDIC. Anything above that will get paid out before other creditors and stockholders — who generally get nothing when a bank fails — and recovery levels vary. Washington Mutual depositors got all of their money back when that bank failed in 2008, while depositors at IndyMac, another failure that year, got 50 cents on the dollar, according to FDIC records.

Concerns have quickly shifted to other banks that might be in trouble. First Republic, another West Coast-based bank whose shares are down more than 30% since Wednesday, tried to reassure investors. In an unusual statement midday Friday, it said tech companies only account for 4% of its deposits and that less than 15% of its total assets are invested in securities like bonds.

Liz’s view

This isn’t 2008 and the blast radius, while it likely won’t stop with SVB, isn’t likely to be systemic. For one thing, the bad bets at the heart of this collapse weren’t on toxic real estate securities but largely plain-vanilla bonds — most of them Treasury bonds — that can be easily valued and sold.

In 2008, the original plan to buy toxic assets had to be reworked because it simply would’ve taken too long and their value was too hazy to lend against. Here, the FDIC should be able to quickly put a price on what SVB owns and use that to advance money to uninsured depositors, unclogging the system and stemming the panic.

Step Back

SVB, which has said it counts nearly half of U.S. venture-backed tech and life science companies as clients, got a surge of deposits in 2020 and 2021 when startups raised huge sums of money. It invested much of that in bonds paying lower interest rates, whose value has plummeted as the Fed has quickly raised rates.

Most banks saw an influx of deposits, in large part due to stimulus payments and lower spending during the pandemic. What they invested that money in is now a crucial question for the industry and its risk management capabilities.