Semafor/Al Lucca

Semafor/Al LuccaPrices are stubbornly higher and the job market is still on fire. That combo presents a delicate task for the Federal Reserve to raise interest rates without hurting the economy — the soft landing everyone is talking about.

Peter Kraus, the CEO and founder of $4.5 billion Aperture Investors, is skeptical that the Fed is up to the job. The former CEO of AllianceBernstein and a 20-year veteran of Goldman Sachs is bullish on China, though. We talked about opportunities abroad and concerns at home. Here’s our conversation, edited for length.

Q: January marked the lowest unemployment rate since 1969, which could push the Fed’s interest rate to above 5% this year. Where are you on its ability to pull off a soft landing?

A: I don’t believe in the soft landing myth. If I had $100, I might bet $2 or $3 on that, but I’m not betting $50. The credit event that I see happening is unlike what we experienced in the previous two market downturns, in 2008 and 2020.

Q: How so?

A: We went from a 35-year stretch of declining inflation, and increasing technology and efficiency to a world where you still have that increasing technology and efficiency, but with inflation. Inflation at 3% is not bad. You’re not going to jail for 3% inflation.

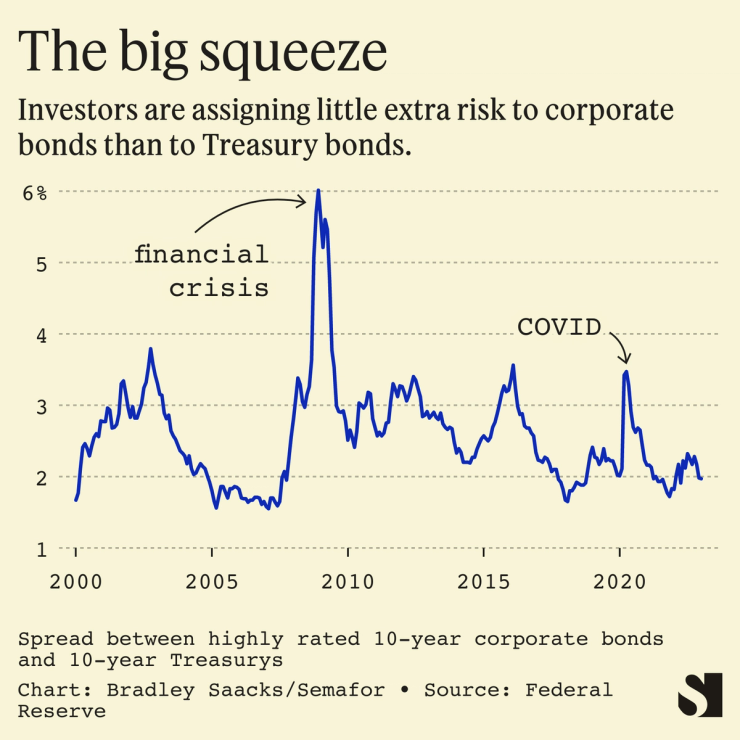

But the 10-year Treasury is going to be at 4.5%. And you’re going to borrow 350 to 400 basis points over that. So when companies refinance, they will have to raise at double the interest rate. Some will have to restructure, either by selling equity or by reorganizing in bankruptcy. I don’t think the market is pricing that in. [Credit] spreads need to widen.

Even in a soft landing, where there’s no recession but very slow growth, you’re going to still have this refinancing problem. The only way this all works is that you have slow enough growth and inflation that the Fed cuts rates. I don’t think it can’t happen. I just don’t think that it’s a high probability.

I would look at a high-risk bond today and say, ’You’ve got to pay me something to account for the five out of 10 scenarios where life gets really bad.”

Q: Tensions between the U.S. and China have been rising over technology, Taiwan, and now the spy balloons. You wrote recently that being underinvested in China is a bigger risk than being overexposed. Why?

A: The risk premium you need to be paid to be in China has gone up. It’s not COVID, it’s the government. It was always possible that they would get belligerent over Taiwan, but it wasn’t in the paper every day. You look at China today and say you have to pay me more for an asset there than for an identical asset in Germany. Three years ago, that difference was not that big.

But China is cheap enough to still take that risk. Still, it’s not going to go back to what it was unless the government changes its policies.

Q: You’ve also mentioned a trip to the Middle East where you see “more growth potential” than anywhere else in the world. Why are you so bullish?

A: I’ve been going to the Middle East for 25 years. The speed at which it’s grown in the last three years is really remarkable.

In addition to that, the Middle East obviously has no water. And so if you’re going to provide water to a population in a desert, density matters, because you can’t lay water pipes all through the Saudi Arabian peninsula. But you can send it all to Riyadh.

And when you put more people in one place, it’s easier for the dry cleaner business to be successful, for the movie theater to be successful, for the food court to be successful. Once the services start to grow, then you get kind of a middle class and businesses that are not just being driven by government spending.

Q: Your firm charges investors in its mutual funds a lower base fee but higher performance fees. But retail investors and their advisors haven’t taken to it. Why not?

A: I think they don’t do the math. They look at a performance fee, and say, ‘That’s expensive, I don’t want to pay that,’ even though they don’t pay it unless we perform. We have to actually beat the benchmark. Large institutions, they understand it. But the retail investor is being sold to by a financial advisor, and advisors don’t want to take the time to understand this and explain it to their clients.

Q: Let’s end on something fun. You’re a big art collector. Do you still believe in digital art in the form of NFTs (non-fungible tokens)?

A: NFTs are a viable way to democratize the value of art ownership. They are in their infancy, and volatility is to be expected. If it doesn’t calm down, though, their utility could fall to a level where investors lose interest. The market will become non-functional. That said, I’m always excited about new artists that are making new imagery. But that’s not very newsworthy.