Amena’s view

When it comes to managing oil markets, the focus typically falls on OPEC and its efforts to regulate supply. Yet with the Strait of Hormuz effectively closed for more than three months and roughly 12 million barrels per day of OPEC+ production shut in, market balancing has taken on a very different form. An increasingly important question has emerged: can oil markets also be managed through the demand side of the equation? China, the world’s largest crude importer, is demonstrating that they can — at least temporarily.

Over the past 18 months, China’s aggressive build-up of its strategic petroleum reserves attracted considerable attention. Analysts debated Beijing’s motives, ranging from energy security concerns to expectations of future geopolitical disruptions. For major oil exporters, however, the reasoning mattered less than the outcome. Chinese purchases provided a crucial source of demand during a period of oversupply, helping to establish a floor under prices and to counter narratives of a global glut. Now, with Hormuz flows heavily restricted, China’s decision to sharply reduce imports has become an equally important factor in market fundamentals.

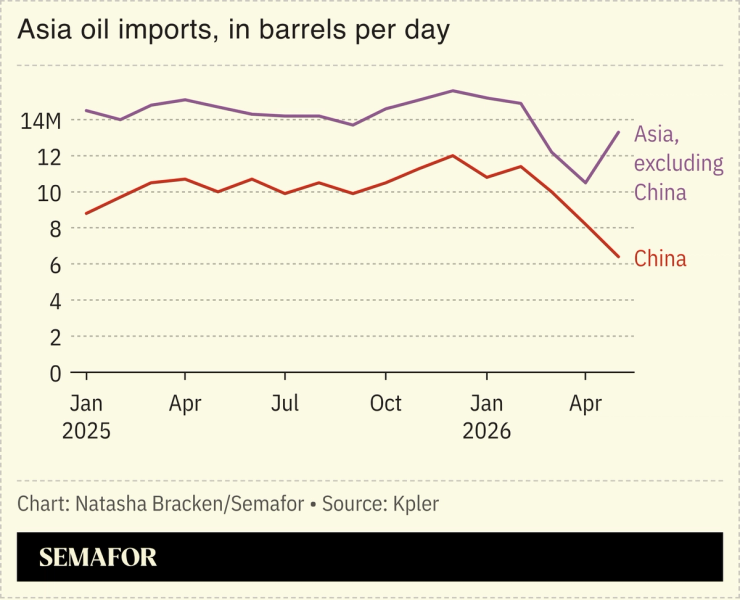

In May, China’s seaborne crude imports fell to around 6.7 million barrels per day, their lowest level in a decade according to Kpler, the independent data provider where I work. Imports were down by approximately 3.5 million barrels per day year-on-year. Chinese refinery runs have also declined to roughly 13.1 million barrels per day, about 1.8 million lower than a year earlier.

Part of this import decline is being offset through inventory management. While strategic petroleum reserves have actually increased by around 8 million barrels since the conflict began, refinery inventories fell by roughly 15 million barrels in May alone. Refinery storage remains slightly above 300 million barrels, providing an estimated 60–75 days of cover at the current import rates. This inventory drawdown could allow China to maintain depressed import levels until around August. Beyond that point, however, refinery inventories will need to be replenished, limiting China’s ability to continue acting as a demand-side shock absorber.

China’s behaviour is not purely driven by market considerations. Its strategy also carries geopolitical implications. China has strong incentives to preserve its long-term access to Iranian crude and maintain its influence with a key regional supplier. By reducing purchases while avoiding meaningful pressure on Tehran to reopen the Strait of Hormuz, Beijing is giving Tehran more time to sustain pressure on Washington.

The combination of Chinese demand restraint, inventory drawdowns, strategic stock releases, and the rerouting of crude flows are why oil is not currently trading at $150 per barrel. However, they are temporary coping mechanisms rather than lasting solutions. The longer the Strait of Hormuz remains disrupted, the greater the risk that the available buffers will be exhausted.

Even if conditions improve, restoring Middle Eastern production will not be immediate. Saudi Arabia and the UAE could likely bring back substantial volumes within three to four weeks, but Kuwait and Iraq may require four to five months to fully restore output. Full normalization would also depend on mine clearance operations, reduced military threats, the return of insurance coverage, and the availability of sufficient tanker capacity. Even then, a complete recovery of regional supplies may not occur until well into 2027.

What matters is not whether the market appears balanced, but how that balance is being achieved. Before the disruption, global oil flows depended on the continuous movement of crude through Hormuz. Today, equilibrium is being maintained through demand erosion, inventory depletion, emergency stock releases, and increasingly complex logistical workarounds. These mechanisms can mask tightness for a time, but they do not eliminate it.

Until a meaningful portion of disrupted supply returns, global balances will remain vulnerable. For now, the market has proven far more adaptable than many expected, myself included. But as inventories continue to decline and Chinese imports eventually normalize, the market will become increasingly dependent on the pace of Middle Eastern recovery. The exact point at which today’s temporary adjustments stop working is difficult to predict. What is clear is that they cannot last forever.

Amena Bakr is the Head of Middle East Energy & OPEC+ research at Kpler, an independent global commodities trade intelligence company.

Notable

- Falling Chinese oil imports are shielding the global market from higher prices, according to traders and analysts cited by the Financial Times.