The News

Last year was hellacious for big U.S. and European offshore wind companies. But their latest results offer some cautious optimism that the worst may be over, that they are tightening their belts, and taking baby steps toward profitability.

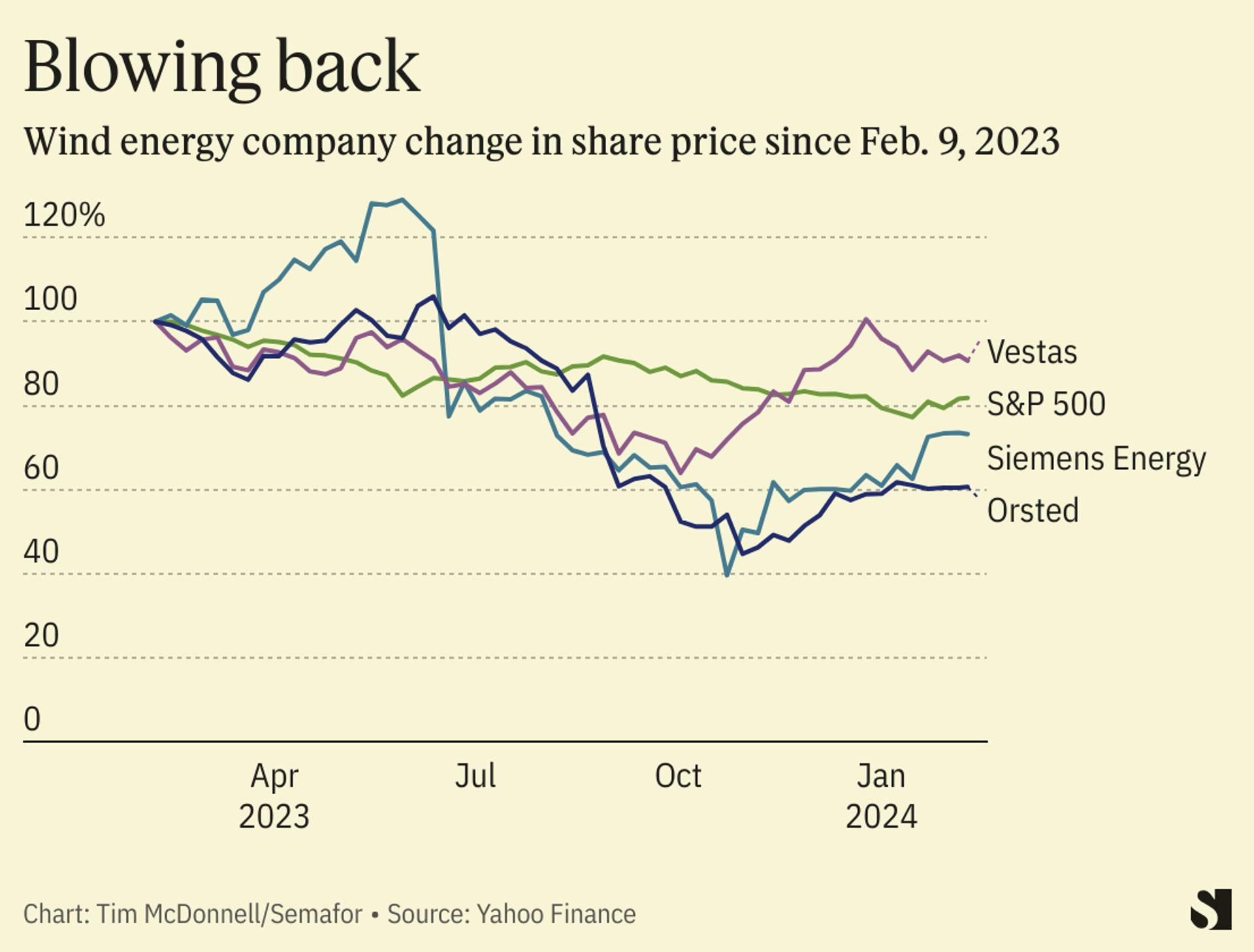

In annual earnings reported this week, Danish wind farm developer Orsted posted a net loss of $2.9 billion for 2023, cut 9% of its workforce, and said its chairman would step down after a decade. Siemens Energy warned its turbine-manufacturing subsidiary was still dragging the company down with hundreds of millions of dollars in losses. And Vestas, despite turning a profit, suspended its dividend payments. But each also offered kernels of good news for investors, with Orsted curbing spending, Siemens closing in on offshore wind profitability, and Vestas offering a better profit outlook for 2024 than Wall Street had feared.

Tim’s view

Offshore wind has a chance for a reset, both because of actions executives are taking to stem their losses, and because of improving market conditions.

Building offshore wind farms is expensive and slow, and every company in the business has faced the same basic problem: Contracts signed a couple of years ago — either for the installation of hardware, or for the delivery of electrons to the grid — no longer reflected manufacturers’ and project developers’ real costs, thanks to rising costs and supply chain disruptions. Margins evaporated, and companies like Orsted decided it was better to eat government fees for canceling projects than to forge ahead with no profit.

That imbalance is starting to even out. For one, the environment is improving. Interest rates may fall this year, particularly important for offshore wind, because companies often borrow to make huge upfront capital expenditures. Governments are also beginning to reset their expectations. At an auction in January, New York agreed to pay higher prices for offshore wind power, drawing big developers like Equinor back into the game. The U.K. plans to boost its subsidies for the sector by two-thirds. Manufacturers, too, are setting higher prices and passing more of their costs on to developers. Vestas managed to ride that strategy to a profit and still book its highest-ever quarter for new orders. Globally, 25 gigawatts of offshore wind projects are expected to start construction in 2024, according to Rystad Energy, almost double that of 2023.

Companies are also resetting their own expectations, and getting a handle on spending. Orsted’s strategy for recovery involves retreating from several years of speedy growth. The company suspended its dividend payments, halved its planned investments, and lowered its total renewables installation target for 2030 from 50 to 38 gigawatts. It also plans to call off potential projects in Norway, Spain, and Portugal. But CEO Mads Nipper said the company was still keen to pursue projects in the U.S., particularly for those with low upfront costs and with power delivery contracts that protect the company from inflation. Orsted clearly thinks that moving early into the nascent U.S. market will ultimately be worth a few years of instability.

For equipment manufacturers like Vestas, the most important step is to clear out the backlog of old, badly-priced contracts to better reflect higher costs for steel and other raw materials. Deutsche Bank analysts downgraded Vestas stock from “buy” to “hold” in a research note last week, in large part because the company remains weighed down by a backlog that will take at least another six months to clear out. There’s not much manufacturers can do to avoid those losses except try for better terms in new contracts, said Samantha Woodworth, senior wind analyst at Wood Mackenzie: “Unfortunately, this is going to be a bitter pill for them to swallow.”

And it’s going to take a few years to go down: Siemens doesn’t expect its offshore wind division to turn a profit until 2026.

Room for Disagreement

The more that companies like Vestas raise their prices, the more of a squeeze they put on developers like Orsted, a self-defeating cycle that some analysts warn is unsustainable without more government intervention. Meanwhile, other headwinds for offshore wind haven’t gone away. Costs are still rising, wholesale power prices are falling, and infrastructure permitting and grid interconnection worldwide remain painfully tedious. This year “will not be a year of magic” for offshore wind, Coco Zhang, ESG analyst at Dutch bank ING, told me. Siemens Energy expects to lose money in 2024, in part because its offshore wind turbine orders were lower than expected, something that may be the result of bad press surrounding quality problems with some of its wind hardware. British oil major BP said this week that it wrote down the value of its foray into U.S. offshore wind by $1.1 billion. The company is in no rush to try the U.S. again, new CEO Murray Auchincloss said, adding that he plans to steer clear of any offshore wind deals predicated on fixed delivery contracts with utilities.

The biggest wildcard is the U.S. election. Donald Trump is an outspoken enemy of offshore wind, and if he gets re-elected, the effect on the U.S. offshore wind industry could be “catastrophic,” a top Biden administration energy permitting official warned this week. That risk may keep investors from gambling on many big new projects this year.

The View From China

The outlook is much cheerier in China, by the far the world’s biggest offshore wind market. The country controls much of its wind supply chain, and enjoys far lower production costs and a more streamlined energy infrastructure bureaucracy. This week, a Chinese company broke the world record for the longest wind turbine blades ever manufactured: 131 meters, 1.5-times the height of the Statue of Liberty.

Notable

- A fight is brewing off the coast of California about whether part of a sensitive habitat for marine mammals should be left out of a federal wildlife sanctuary in order to leave it clear for offshore wind infrastructure.